Machinery purchases

Author: James Hagan and Tamara Alexander (Department of Agriculture and Food, WA) | Date: 23 Mar 2015

Take home messages

- When considering machinery options, farmers should not only consider the capital cost of the equipment but also consider their seasons, the risk of delays to seeding, spraying or harvest and the associated penalties and then assess the overall financial impact of each machinery option.

Important disclaimer

The Chief Executive Officer of the Department of Agriculture and Food and the State of Western Australia accept no liability whatsoever by reason of negligence or otherwise arising from the use or release of this information or any part of it.

Copyright © Western Australian Agriculture Authority, 2015

Making the decision

New grain harvesters can cost in excess of $500,000, and are just one of the many important capital expenditure decisions that farm businesses will make. Should a farmer always own their own gear? What are the alternatives? What factors should farmers consider when deciding their investment in harvesting, seeding and spraying machinery and the capacity that they require? This paper will canvas these issues.

The factors to consider when deciding about investment in machinery capacity include (but are not limited to):

- Cost, availability and reliability of contractors.

- Cost and availability of leasing or renting equipment.

- Cost of complementary investment to reduce logistic delays such as additional on-farm storage, another chaser bin and/or increased use of haulage contractors.

- Costs and problems with sharing a machine or implement with a neighbour.

- Financial cost of delays to harvest, or seeding, e.g. fire risk, weather damage, yield penalties and grain quality downgrades.

- Skills you have in maintaining and repairing machinery, or availability of mechanical expertise should it be required.

- Cost of new versus second-hand equipment, and expected lifespan of that equipment.

- Size of both your current and future cropping programs and seasonal conditions.

- Opportunity cost of using capital that could be allocated elsewhere.

Decisions on investment in machinery should be based around what the business can afford (profitability), how much additional revenue/cost savings the new or upgraded machinery can generate and does this additional value justify the additional cost.

An upgrade or purchasing new equipment may have some benefits (e.g. time) but may not create sufficient new income or cost savings to justify the higher machinery cost. In some cases, it may be appropriate to place a risk weighted value on benefits that are difficult to quantify (e.g. cost of failure x probability of failure occurring = potential cost savings of upgrading).

Owning versus operating costs

The total cost of machinery is the sum of the capital costs and the operating costs.

| Machinery cost = Capital costs + Operating costs |

Machinery capital costs are referred to as fixed, or ownership costs. They are the annual costs incurred regardless of whether the machinery is used or not. Capital costs include the change in capital value of the machinery over time, opportunity cost of capital invested in machinery; and insurance, registration and shedding costs.

| Capital costs = Change in Capital value + insurance + registration + shedding + opportunity cost of capital |

The opportunity cost of capital is the return that could be generated from an alternative investment (e.g. bank deposit).

The annual change in capital value is the annual cost of the machine over its intended life on the farm. It is the purchase value of the machine, minus its resale value, divided by the years it will be in operation for before resale.

| Annual change = Purchase value – Resale value

in capital value Years of Service |

It is worth noting that even though a piece of machinery may have depreciated to zero value for tax purposes over a period of time, if it is still being used then it is not worth zero to you, and you need to account for this.

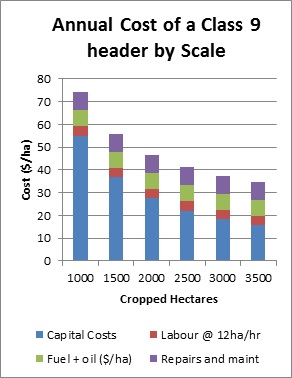

Example: For a new Class 9 harvester, which is purchased for $500,000 and sold seven years later for $150,000 the annual change in capital cost equates to $50,000/yr, the cost of insurance (typically 1% value), shedding, registration and opportunity cost is then added to this value to calculate the full capital cost. All for the privilege of owning a harvester, before it has been used. Figure 1 shows how this cost of ownership (capital costs) can be made more efficient the greater area a machine works.

Figure 1. The cost breakdown of owning and operating a class 9 header by cropped hectares.

The operating costs are the costs of operating the machinery and include all consumables, fuel, labour, general repairs and maintenance. The annual operating costs increase with machinery usage however will remain constant on a per hectare or hour basis (i.e. more hectares will not lower the $/ha cost) as shown in Figure 1. The cost of operation should include a labour cost, whether the operator is family or hired.What benchmarks can be aimed for in respect to machinery investment?

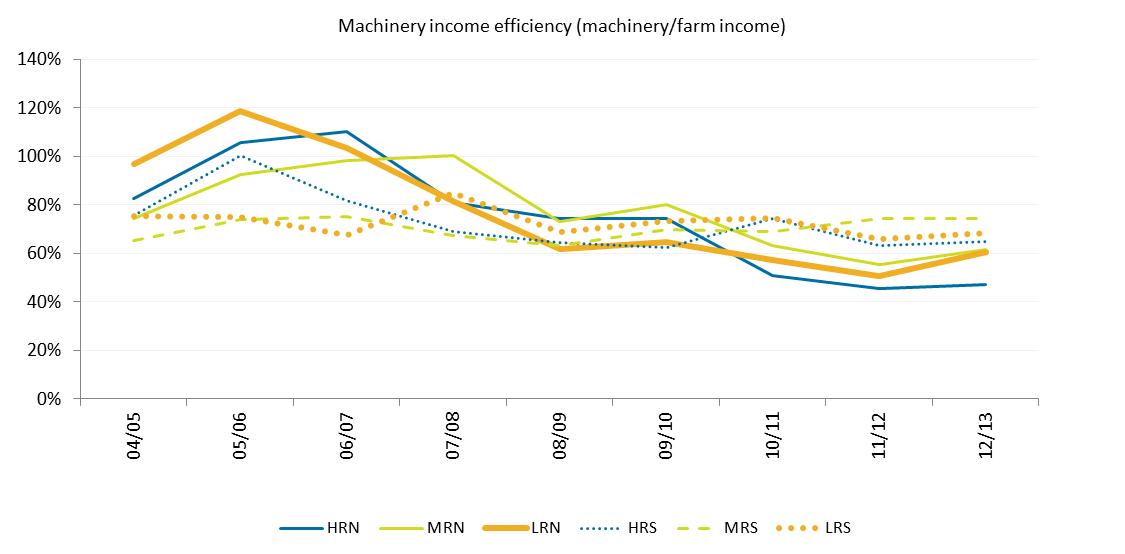

Machinery income efficiency is an indicator that reflects the ratio of machinery assets to farm income. It is a whole-of-business benchmark that provides a guide to the typical amount a farm business can invest in owning machinery. It is calculated by:

| Machinery income = Total machinery assets in capital value Total farm income |

Where Total machinery assets is the current market value of all machinery, and;

Total farm income is the average farm income over the last four years.

As a benchmark, average machinery income efficiency for producers in WA is around 0.6 and has been trending down as efficiency has improved (Figure 2).

This ratio indicates that farms have the equivalent of around 60% annual income, on average, tied up in machinery/plant capital or, to put it another way, the farm is generating $1.67 income on every $1 investment in machinery/plant.

Please note that this ratio should not be acted on in isolation. It does not account for other factors that influence the cost of machinery such as operating costs, use of contractors, hired equipment and the livestock/cropping enterprise mix. For example, if machinery is old or hired the machinery income efficiency may be very low and appear healthy but the operating costs may be very high reducing profitability or productivity. Hence to analyse how much to invest in machinery the business must understand and analyse the full cost of machinery (capital and operating), cost of alternatives and opportunity cost of under-investment (e.g. delays)

Figure 2. Machinery income efficiency ratio by rainfall zone in WA using zone averages.

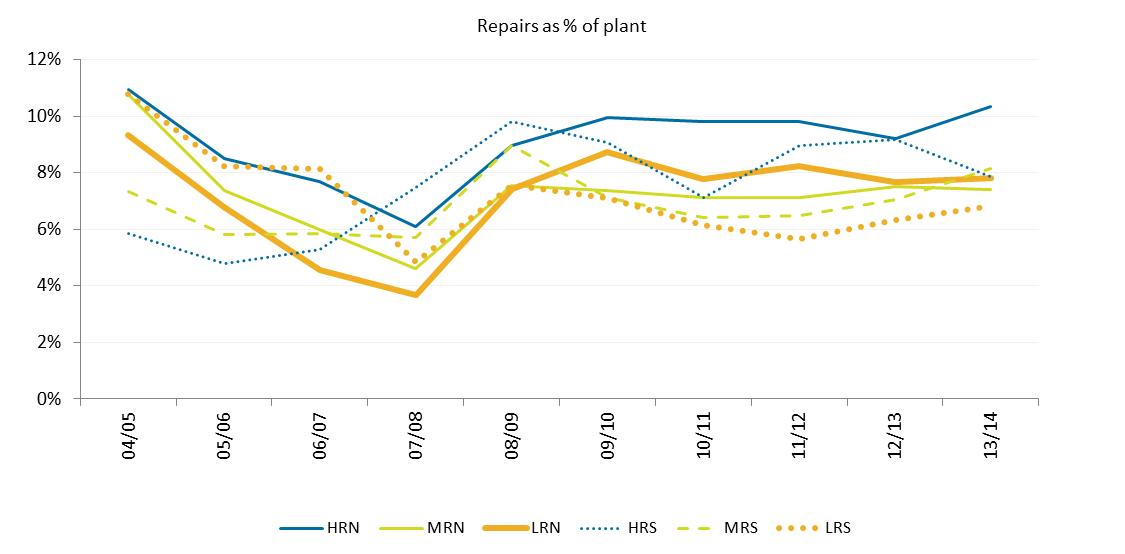

Another indicator to consider benchmarking is the cost of repairs and maintenance as a percentage of plant or machinery value. Figure 3 highlights that, on average, expenditure on repair and maintenance accounts for around 7-8% of the farm’s plant value (majority is machinery) for producers in WA.

Figure 3. Repairs as a percentage of plant value by rainfall zone over time in WA calculated from Bankwest Planfarm benchmarks.

Machinery expansion

Expanding machinery capacity needs careful consideration. Is the reason for needing to upgrade capacity profit driven, lifestyle driven or event driven?

The cost, efficiency and potential bottlenecks across each farm business’s logistics set-up in season and at seeding and harvest needs to be analysed before and after a potential investment in expansion. For instance, efficiencies of a second header may not be generated unless investment is also made in freight, storage and handling to avoid bottlenecks and delays in logistics. Hence, the cost of further investment needs to be included if the assumption is for high utilisation of the second harvester. If not, lower utilisation and costs of delays/waiting time and additional labour needs to be factored in when calculating the true benefit of the potential purchase. If timing is critical, such as the seeding window, the cost of not meeting the critical window needs to be quantified (yield penalty x price x hectares in late) and compared to the additional cost of investing in upgraded or additional machinery.

Furthermore, assessment of the likelihood of a range of seasons needs to be considered. For example, expanding capacity for a one-in-ten year event may lead to an overinvestment of capital that may have generated higher returns if invested in another part of the farm business.

Every farm business has different risk exposure, enterprise mix, market options and harvest arrangements. Variations include distance to port, distance to domestic buyers, area cropped, livestock mix, impact economics of storage and risk of quality downgrades, experience of labour, agreements with local contractors, scale of operation and weather conditions, etc.

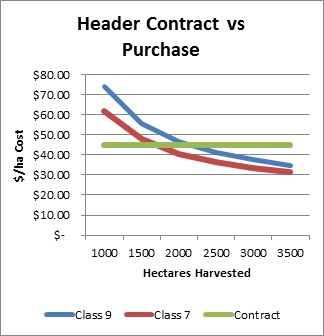

The investment in a new harvester is significant and can cost up to $80,000 per annum in fixed costs. By comparison, operating costs are relatively minor on new equipment. Often a new purchase cannot be justified for smaller cropping programs or a farm that has expanded the crop area but not by enough to justify purchasing another harvester or seeder. Other options are available, such as buying second hand, buying a chaser bin, equipment hire, share-farming, contracting or if larger machinery is purchased contract it out (Figure 4). Each of these options has its particular advantages and costs.

Purchasing a new harvester is not the only way to invest in harvesting capacity nor is it the only investment consideration at harvest. Other investment decisions that may be considered at harvest include investment in chaff carts or seed destructors, haulage trucks, chaser bins, field bins, silos, sheds, sausage bags, labour, etc.

Figure 4. Contract versus owned harvest costs by hectares harvested at 12ha/hr.

Another issue at harvest is the consequence of bottlenecks in the regional supply chain, particularly in seasons with above average yields. When regional grain production is very large, contractor harvesters, rental equipment and transport trucks can be in short supply and the turnaround time at the grain bins is often significantly longer. If it appears the season will result in delays in turnaround time and there is a risk of an adverse weather event and possible downgrade, we recommend farmers consider investing in additional on-farm storage. Similar to the supplementary contracting scenario, a downgrade in quality can cost a lot more than the investment in additional storage such as silos, sausage bags or sheds.

Conclusion

In summary, when considering machinery options, farmers should not only consider the capital cost of the equipment but also consider their seasons, the risk of delays to seeding, spraying or harvest and the associated penalties and assess the overall financial impact of each machinery option. In general, be aware of the often high fixed costs of buying a new machine, match it with the ability of the farm enterprise to absorb this overhead and also consider the opportunity cost of alternative uses of the capital.

Contact details

Tamara Alexander

Senior Economist, Narrogin

(08) 9881 0225

tamara.stretch@agric.wa.gov.au

James Hagan

Economist, Geraldton

(08) 9956 852

james.hagan@agric.wa.gov.au

Was this page helpful?

YOUR FEEDBACK